PS đi xuống sau 4 tháng tăng giá ở châu Âu

PS đi xuống sau 4 tháng tăng giá ở châu Âu

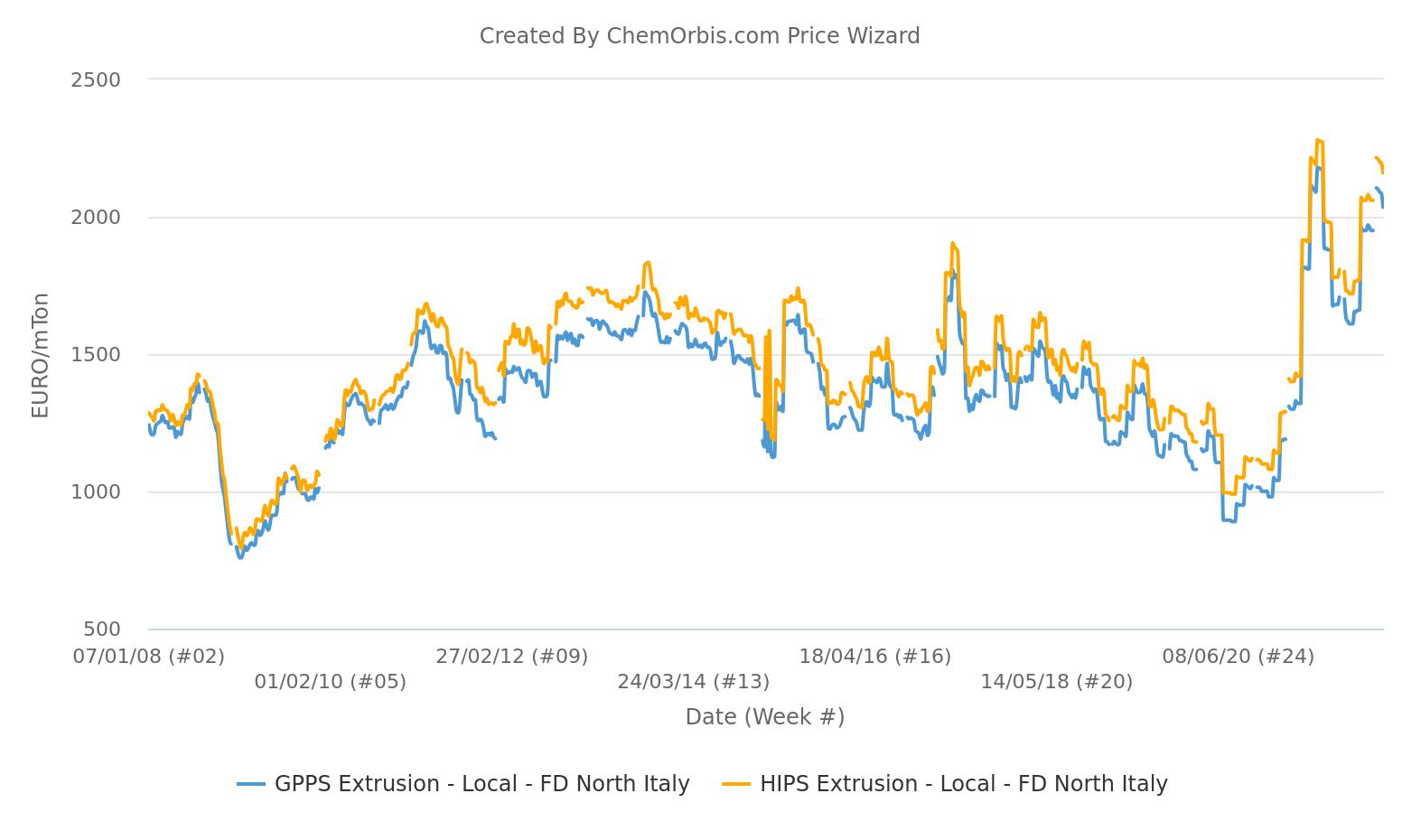

Trong biểu đồ dưới đây, giá tại Ý vẫn đạt mức cao nhất mọi thời đại, với bối cảnh tương tự ở Tây Bắc Âu. Chỉ riêng điều này đã mở đường cho dự báo chứng kiến các đợt điều chỉnh giảm giá trong những tuần trước mặc dù thị trường thượng nguồn cực kỳ biến động.

Trước khi giá PS đảo chiều vào tháng 2, chúng đã có xu hướng leo dốc kéo dài từ tháng 10 năm 2021 đến tháng 1 năm 2022, được hỗ trợ bởi sự gia tăng chi phí và tình trạng khan hàng. Theo Chỉ số Giá ChemOrbis, giá giao ngay trung bình hàng tháng đã tăng ít nhất 25% từ đáy đến đỉnh.

Đà giảm giá PS bằng hoặc vượt qua mức giảm của styrene

Mức thanh toán styrene thấp hơn rõ ràng là lý do chính sau chính sách giảm giá của người bán trong tháng 2. Mức thanh toán hợp đồng hàng tháng theo sau các hợp đồng benzen thấp hơn do sự biến động chi phí năng lượng.

Hai nhà sản xuất styrene lớn đã công bố báo giá PS ở mức thấp hơn 40-70 EUR/tấn so với tháng 1, trong khi mức giảm 50-70 EUR/tấn được thị trường chứng kiến một cách thường xuyên hơn. Một nhà sản xuất lớn cho rằng việc chiết khấu lớn hơn mức giảm styrene là do sự sụt giảm giá năng lượng trong tháng 1.

Những mối lo ngại về nguồn cung giảm bớt do công suất trở lại, nhu cầu suy yếu

Mặc dù nguồn cung vẫn chưa cải thiện đáng kể, song nhiều người tham gia thị trường dự đoán sẽ chứng kiến sự gia tăng mức cung do các nhà sản xuất trong khu vực đã dỡ bỏ các trường hợp bất khả kháng và tiếp tục sản xuất tại các nhà máy PS của họ. Một số người mua, những người đã mua nguyên liệu nhập khẩu trong những tháng qua, đang chờ đợi sự cập bến của những lô hàng này.

Người mua dường như ít quan tâm hơn đến nguồn cung bất chấp tình trạng giao hàng chậm trễ và thiếu tài xế xe tải cản trở việc di chuyển từ và đến khu vực.

Về mặt cầu, có một chút lạc quan về các hoạt động bổ sung hàng tồn kho. Giá cả vẫn leo thang gây cản trở người mua trong việc mua hàng nhiều nhất có thể.

Trong những tháng qua, nhu cầu mạnh hơn chủ yếu là do thiếu hụt nguồn cung và người mua chỉ cố mua hàng do giá cả tăng cao và dự báo giá giảm thêm.

Trong phân tích dựa trên sản phẩm, nguồn cung HIPS eo hẹp hơn, hỗ trợ nhu cầu đối với loại nguyên liệu này. Trong khi đó, GPPS chứng kiến sự hỗ trợ từ các ứng dụng cách nhiệt.

Đối với lĩnh vực đồ dùng một lần, lượng tiêu thụ GPPS đang dần chậm lại trái với niềm tin phổ biến rằng nhu cầu giảm mạnh trong năm 2021. Trong khi đó, theo Chỉ thị SUP, các nhà sản xuất Ý sẽ có thể sản xuất các mặt hàng sử dụng một lần được làm từ các thành phần có thể phân hủy sinh học hoặc có thể phân hủy thành phân ủ.