Thị trường PP, PE và PVC của Thổ Nhĩ Kỳ khép lại tháng 5 với xu hướng giảm giá, điều gì sẽ xảy ra trong thời gian tới?

Thị trường PP, PE và PVC của Thổ Nhĩ Kỳ khép lại tháng 5 với xu hướng giảm giá, điều gì sẽ xảy ra trong thời gian tới?

Giá PP, PVC và PE đã tiếp tục đi xuống khi thời điểm cuối tháng 5 gần kề. Các thị trường đã sẵn sàng kết thúc tháng này với xu hướng giảm giá dưới tác động của nhu cầu yếu vì áp lực lạm phát cũng như thanh khoản eo hẹp. Trong khi đó, những người tham gia thị trường đã bắt đầu tập trung vào triển vọng tháng 6.

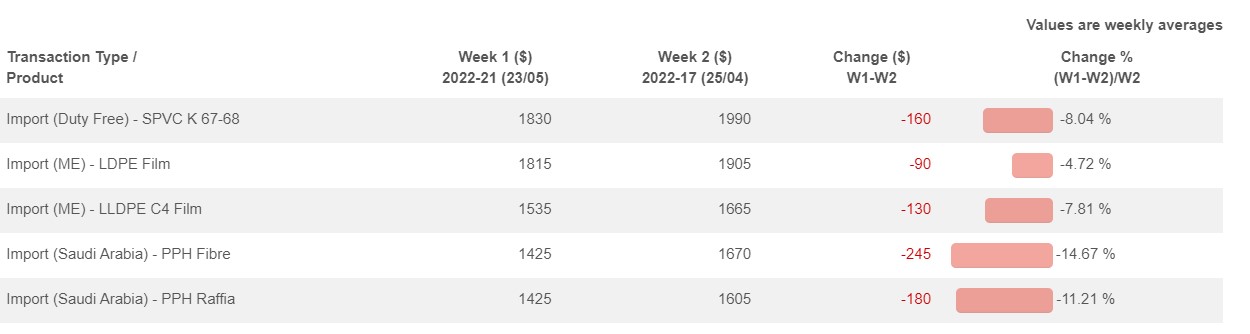

Giá mua giảm dẫn ến đợt trượt giá nhanh chóng của PP homo

Nhu cầu yếu do sức mua thấp hơn và thị trường cuối cùng trầm lắng đã tiếp tục kéo giá PPH nhập khẩu đi xuống trong tuần này. Trong khi đó, tốc độ giảm giá đã khiến một số người tham gia thị trường ngạc nhiên. Họ nói: “Chúng tôi đã dự đoán sẽ không chứng kiến mức giá thấp như vậy trước tháng 6. Điều này chứng tỏ sự trì trệ chung trên thị trường.”

Cả giá PP raffia và fibre của Ả Rập Xê Út ở phân khúc thấp đã chạm mốc 1400 USD/tấn CIF Thổ Nhĩ Kỳ trong một vài giao dịch. Do giá được ước tính giảm 80-120 USD/tấn so với tuần trước, mức giá trung bình hàng tuần mới nhất đã cho thấy mức thấp nhất trong khoảng một năm qua.

Sự sụt giảm này là do xu hướng trượt dốc trên các thị trường PP toàn cầu, nơi người bán khuất phục trước lượng tiêu thụ chậm liên tục ở phía người tiêu dùng cuối cùng. Chi phí propylene giảm cùng với nhu cầu suy yếu đã đẩy thị trường giao ngay của châu Âu đi xuống, trong khi thị trường nhập khẩu của Trung Quốc đã chạm dưới mốc 1100 USD/tấn CFR do ảnh hưởng của tình trạng phong tỏa.

Người bán cho rằng giá có thể sắp chạm đáy sau các đợt giảm mạnh, vì sự lạc quan về việc tái mở cửa Thượng Hải và giá dầu thô kỳ tương lai mạnh mẽ. Tuy nhiên, việc tìm kiếm đáy giá của người bán có thể bị cản trở bởi thị trường hạ nguồn yếu do lạm phát cao và chi phí propylene thấp hơn trên toàn cầu.

PVC chạm mức thấp mới do nhu cầu yếu liên tục

Tương tự, giá PVC nhập khẩu đã tiếp tục đi xuống trong một tuần nữa do sự kết hợp của dự báo giảm giá trong tháng 6 và ngành xây dựng chậm chạp khiến lượng mua hạt nhựa bị giới hạn theo nhu cầu cơ bản. Giá K67 của châu Âu đã giảm xuống 1820 USD/tấn vào cuối tuần, trong khi hàng hóa của Ai Cập và Hàn Quốc đã chạm dưới mốc CIF 1800 USD/tấn.

Dự báo vẫn yếu cho tháng sau trừ khi nhu cầu phục hồi mạnh mẽ. Nền kinh tế biến động và chi phí tiện ích leo thang có khả năng duy trì áp lực lên lượng tiêu thụ hạt nhựa trong nước, chưa kể đến tác động của sự gia tăng tỷ giá USD/Lira. Các hợp đồng ethylene dự kiến sẽ giảm giá ở châu Âu cùng với ảnh hưởng của mùa mưa đối với tiêu dùng của Ấn Độ cũng hỗ trợ quan điểm này.

Tuy nhiên, sự trở lại theo kế hoạch của Thượng Hải sau các đợt phong tỏa do Covid sẽ vẫn được theo dõi sát sao. Các nhà sản xuất PVC Trung Quốc, những người đã tích cực xuất khẩu hàng hóa trong vài tháng qua, có thể tìm được cứu cánh nếu nhu cầu trong nước phục hồi.

Một người tham gia thị trường Thổ Nhĩ Kỳ cho biết: “Các mặt hàng PVC cạnh tranh của Nga và Trung Quốc đã đóng vai trò chủ chốt trong xu hướng giảm giá trong vài tháng qua trong khi hoạt động toàn cầu chịu ảnh hưởng bởi lạm phát cao. Chúng tôi dự định theo dõi liệu dòng chảy này có tiếp diễn vào cuối quý 2 hay không.”

Báo giá PE tháng 6 dự kiến sẽ giảm xuống do nhu cầu mờ nhạt

Giá PE cũng đã duy trì xu hướng trượt dốc, mặc dù thị trường có phần khởi sắc hơn so với PP. Những mối lo ngại về thanh khoản, thị trường cuối cùng trầm lắng vì áp lực lạm phát, và giá ethylene thấp hơn khiến tâm lý đi xuống trong tháng sau.

Hầu hết báo giá của Trung Đông được ước tính giảm 20-50 USD/tấn so với tuần trước, xuống mức 1800-1830 USD/tấn LDPE, 1520-1550 USD/tấn LLDPE C4 film và 1480-1500 USD/tấn HDPE film CIF Thổ Nhĩ Kỳ, chịu 6,5% thuế hải quan, tiền mặt. Báo giá mới từ khu vực này vẫn chưa được công bố. Người mua dự đoán người bán sẽ tiếp tục hạ giá do sự không chắc chắn dai dẳng về nhu cầu và đợt giảm giá tháng 6 từ một nhà sản xuất Ả Rập Xê Út lớn ở Trung Quốc cũng như xu hướng trượt dốc đang diễn ra ở Châu Âu.

Một số người tham gia thị trường đã đưa ra dự báo giá cho tháng tới ở mức 1700-1750 USD/tấn LDPE, 1400-1450 USD/tấn HDPE và 1450-1500 USD/tấn LLDPE C4 film. Một nhà sản xuất cho biết: “Sự gia tăng tỷ giá USD/Lira và những hạn chế về tiền mặt có thể tiếp tục ảnh hưởng đến lượng tiêu thụ hạt nhựa trong nước. Chúng tôi sẽ quan sát hoạt động xuất khẩu dưới tác động của áp lực lạm phát toàn cầu.”